Why didn’t anyone tell me? Ten years as a nonprofit executive, and I never understood the power of appreciated-asset donations. A huge part of my job was raising money and sharing the vision of what God was going through our ministry, but I didn’t understand this concept, which now tells me there was likely free money left on the table (that likely ended up going to the government instead of our nonprofit). I experienced amazing stories of generosity and impact and saw people live out sacrifice in ways I had only previously read stories about, but it wasn’t until relatively recently that I learned that some of my donors could have given significantly more, without digging any deeper into their pockets.

Donating appreciated assets (assets that have increased in value) is one of the most tax-efficient and tax-saving ways to donate to non-profits like yours!

Normalizing the Power of Non-Cash Donations

Most donors know they can deduct a donation from their taxes, but often, even the most generous, well-informed, business-savvy donors don’t realize they can also avoid capital gains taxes if they donate appreciated assets rather than cutting a check or swiping a credit card. When they learn that, along with the associated possible impact of that, it can often lead to bigger gifts.

People can often feel silly when they learn this concept, but they shouldn’t. They’re not alone. “80% of donors own appreciated assets, but only 21% of those donors contributed these types of assets to charity.” That makes it the job of our schools, fundraisers, and financial advisors to make sure this concept is at least known and considered by every single donor we come in contact with.

What’s an Appreciated Asset?

Appreciated assets are simply assets that have increased in value. These can be assets like business shares or interest, homes or other properties like ranches or vacation homes, oil or mineral rights, and most commonly, stock. Every situation is unique and the variables associated with that situation should be evaluated by an appropriate professional – it could be a financial advisor, accountant, or lawyer or the combination of all three, depending on the scenario.

How does it work? - Example

Let’s say your school is doing a capital campaign and a family wants to donate $1 million. First off, what a blessing! But don’t you think the family would like to know that depending on the scenario, there could be an additional ~$200k available to them, just based on the way the donation is structured? The answer is yes.

In the scenario, let’s say the family is selling a $10 million business and they hoped to give $1 million from the proceeds, to the vision and mission of your school. There are two ways to do that:

- Sell, then Give

- Give, then Sell

I’ve illustrated these two options below. Warning, lots of numbers. Some of you might want to skip ahead before you fall asleep.

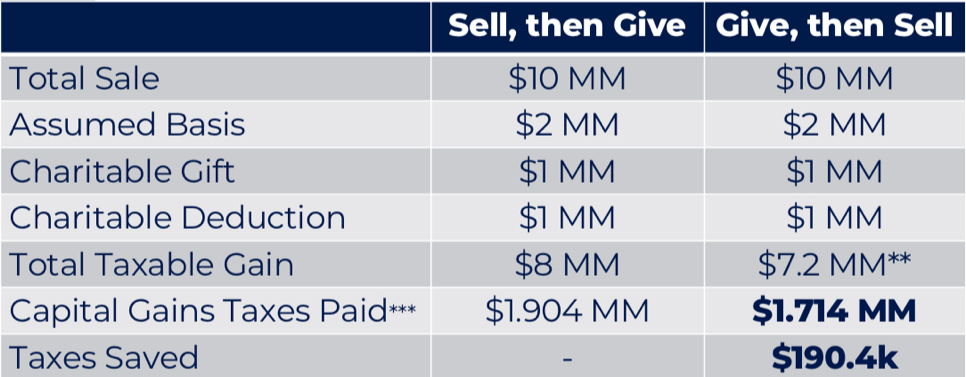

Option 1 - Sell, then Give

$10MM sale. We’re assuming the “basis” (initiate value) of $2MM from years ago, then the company increased in value by $8MM over time. The donor want to give a $1MM gift, which means the donor would get a $1MM deduction on their itemized taxes in either scenario. Focus in here… it’s this part that often gets neglected: the taxable gain. There was an $8MM gain, so there would be a $1.904MM capital gains tax bill on this scenario (assuming the long-term capital gains tax rate of 23.8%).

They’d “give to Caesar what is Caesar’s” - $1.904MM.

Option 2 – Give, then Sell

But when we look at the second scenario, the give-then-sell scenario, which “Caesar” made possible to incentivize charitable giving, if 10% of the company was given before the transaction (ideally before there was even a Letter of Intent to sell), the gain would then be $7.2MM rather than $8MM, which moves the capital gains tax bill down from $1.904MM to $1.714MM. That means, in this very real example, $190.4k of capital gains taxes are saved!

** $800k of gift considered gain, $200k considered basis

*** Long-term capital gains tax rate of 23.8%

Why don’t more donors do it?

How does something like this have so much potential, but relatively so few people understand it? Three main reasons:

- Not as easy as cutting a check or swiping a credit card: Donors have become accustomed to a swift and easy act of donating – they might even get airline miles for it. Some donors will donate through a checking account because it reduces the transaction fees. To change that behavior would require a decent value proposition – in this case, there is one.

- Advisors aren’t always incentivized to help clients give money away – often, financial advisors are paid as a fee on the amount of assets they manage for a client. That would mean that if a client gives money away, there’s less money to manage and a smaller fee to earn. While this incentive structure does keep the advisor aligned with the growth and preservation of resources, when a client desires to give money away, advisors might not prompt ways to creatively give.

- Donors just don’t know – that’s on all of us. We can and should spread the word that if donors want to support our missions financially through a donation, and have any type of appreciated assets, they should at least consider working with a professional to determine whether they could save on taxes, in order to give more to the charitable organizations they love, and often, already support.

The unique role of financial advisors.

Donors are giving this portion of what would be capital gains taxes to someone – and it’s usually the government. Let’s help donors realize that “giving to Caesar what’s Caesar’s” can include giving Caesar less and your school more.

We developed a webinar that has a lot of this same information that can be easily shared here.

If you or your donors have questions about a specific scenario because these scenarios are each unique and often complex, reach out, especially before any appreciated asset is sold. If the asset is sold, or has gone too far down the process of a sale, it might be too late to take advantage of this concept. Send them my way or to an advisor that will help them navigate this. This is my favorite part of my job.

Author, Justin Lopez

Holistic stewardship necessitates that just as much intentionality be focused on what's given away as what’s increased or preserved. Justin has the privilege of working with clients on their “Generosity Strategy”, which includes a family’s giving framework as well as specific ways to maximize the value of their donations.

Justin holds a BS in Industrial Distribution from Texas A&M, where he also played baseball. He now resides in Austin, Texas with his wife, Sally, and their four kids.